- info@srhworld.com

- +91 (20) 24616106 | Helpline : +91 84849 14844

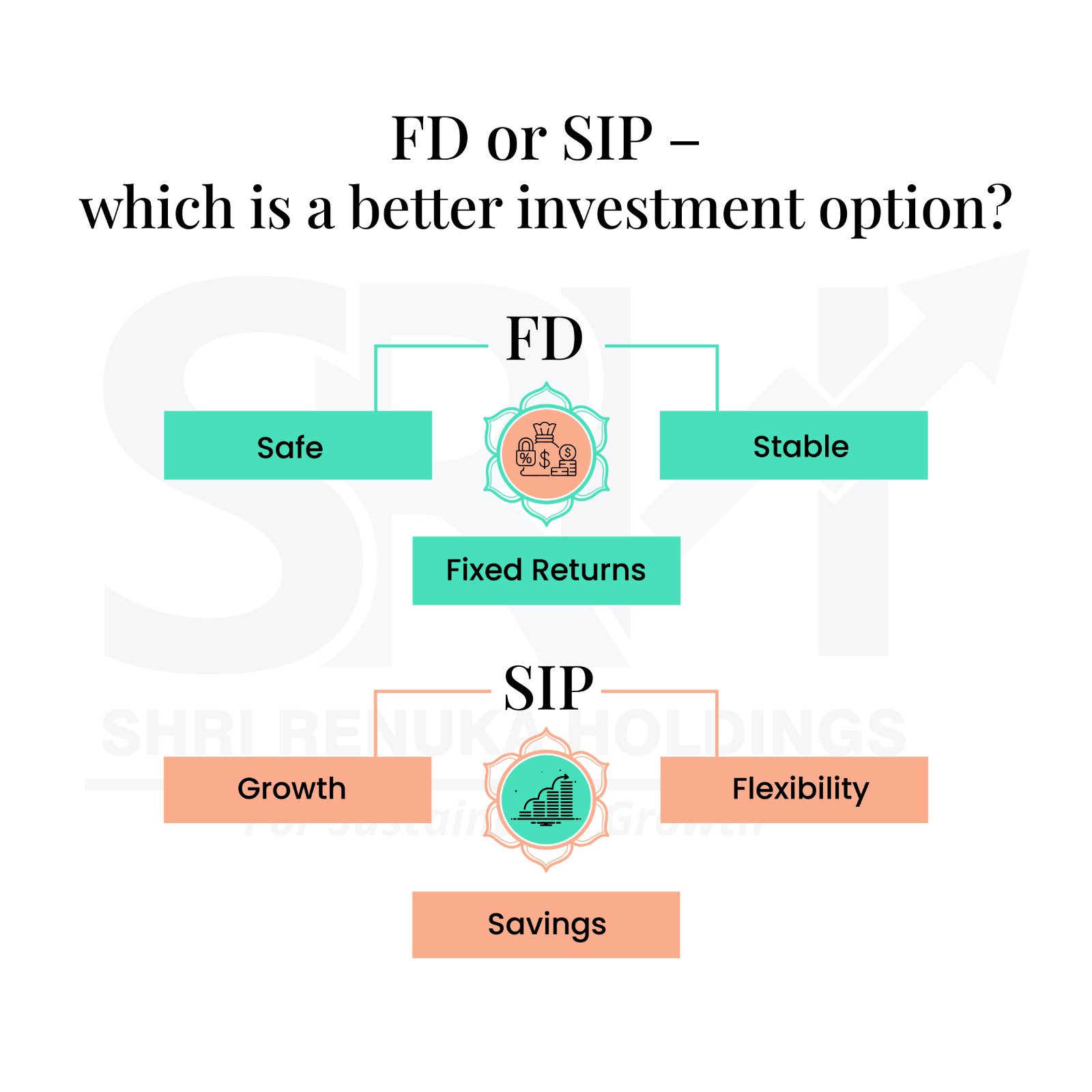

FD or SIP – which is a better investment option?

For decades, FDs have been popular with Indian investors. However, with technical development and financial awareness, investors are seeking more lucrative alternatives that potentially offer higher returns and better control. Mutual fund SIPs have seen a significant rise. However, the question between FD and SIP remains.

Technical development combined with the efforts of institutions to promote financial literacy has increased awareness among Indian investors. Traditionally, investors opted for safe investments like fixed deposits (FDs) that offered assured returns over a fixed duration.

However, today investors have several investment options; one of these being mutual fund schemes offered by asset management companies (AMCs). The AMCs pool capital from multiple investors and the corpus is invested across different asset classes. The schemes are professionally managed by fund managers and their research teams.

What is Fd?

FDs are offered by banks and non-banking finance companies (NBFCs) for tenures between seven days and 10 years. Investors can invest their capital in the FD of their desired duration based on their financial objectives. The interest rate is fixed and any change in the market rate does not impact the returns.

What is a SIP?

When investors opt for a SIP, they choose to invest a predetermined amount in their chosen mutual fund scheme at regular intervals. Generally, the SIPs are goal-oriented and inculcate financial discipline and regular savings.

Difference between FD and SIP

| Particulars | FD | SIP |

|---|---|---|

| Investment nature | Lump sum | Fixed regular instalments |

| Returns | Assured | Based on the performance of the underlying asset class |

| Type of return | Interest on capital investment | Dividend and capital gains |

| Ideal for | Conservative investors with low-risk appetite | Aggressive investors with medium to high risk profile |

| Liquidity | Illiquid; fixed maturity date; premature withdrawal entails penalty | Liquid; amount can be fully or partially withdrawn without any penalty; may have exit load |

| Tax implications | Interest is taxed as per the applicable tax slab | Depending on the type of mutual fund; either short-term or long-term capital gains tax is applicable |

FD or SIP?

FDs are investment tools while SIPs are an investment process, which is done in regular intervals and a comparison may not be completely accurate. Both these options have their pros and cons and investors may opt for either based on their financial goals, risk appetite, and investment horizon. Here are a few things to consider:

🔹 Conservative investors unwilling to risk their capital may opt for FDs while more aggressive investors willing to assume moderate to higher risk to earn greater returns may choose SIPs

🔹 FDs may used to invest a lump sum surplus while investors who want to invest a smaller amount periodically may choose SIPs

🔹 Investors who want assured albeit lower returns may choose FDs while investors aiming for goal-based investments with potentially higher returns may opt for SIPs

🔹 Individuals who have a fixed investment horizon and would not require the funds may choose FDs while individuals who are not sure about their investment duration and require liquidity may opt for SIPs

FDs and SIPs are both investment vehicles that generate returns on the invested capital. Each option has its unique features and suits different investment needs. To choose between FDs and SIPs, consult an experienced advisor at SRH today.

Our journey over 18 years

350 clients across the world

1080 complete projects

22 experts on board

Key Partners