- info@srhworld.com

- +91 (20) 24616106 | Helpline : +91 84849 14844

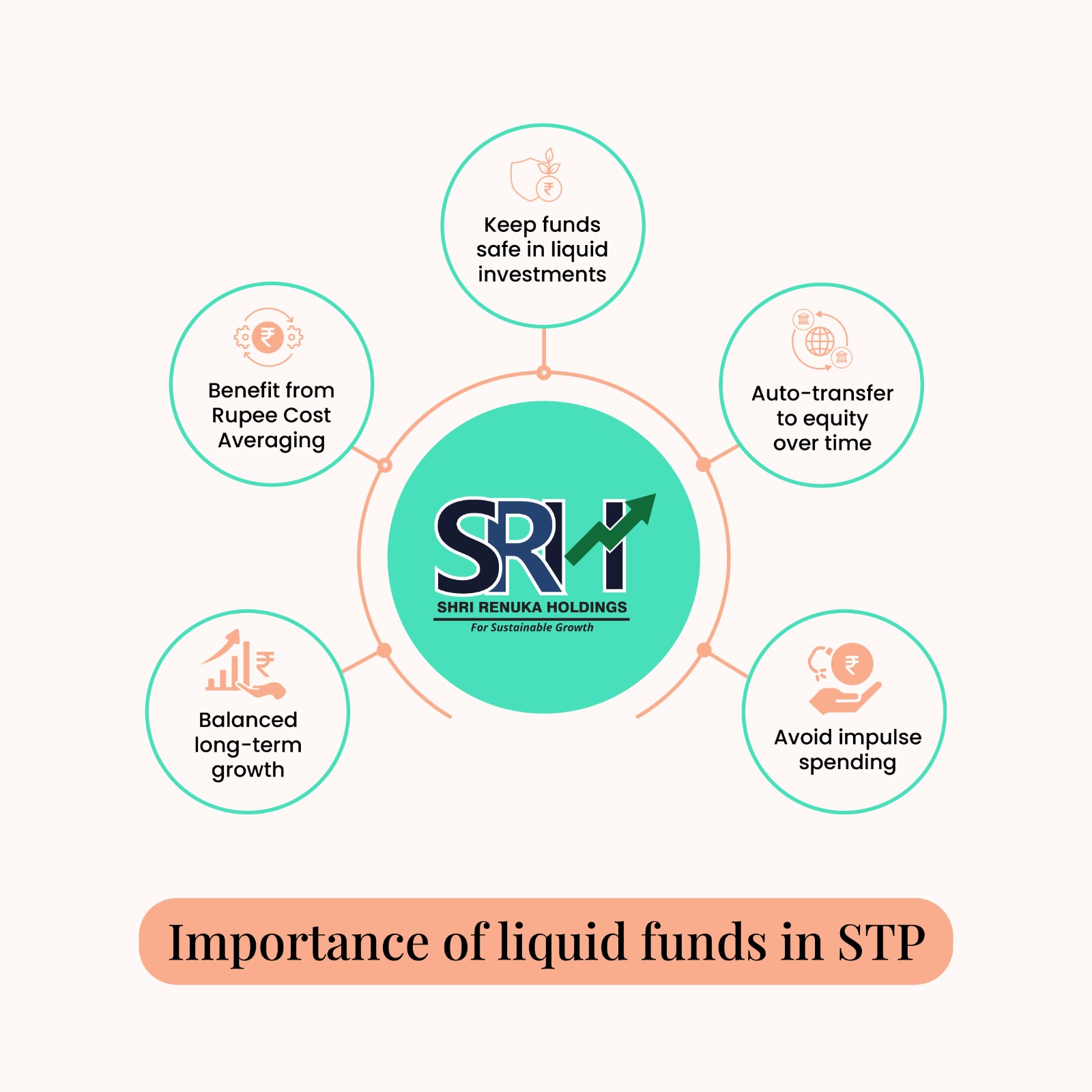

Importance of liquid funds in STP

Most investors are aware about systematic investment plans (SIPs) and its benefits. SIP offers rupee cost averaging and inculcates the habit of disciplined savings. But what happens if you have a lump sum surplus? Is it the right time to invest in equity funds or should you delay the decision? The simple solution to this is STP.

When an individual has a lump sum amount to invest, timing the market and buying at the bottom is almost impossible. A more attractive option is choosing a systematic transfer plan (STP). A STP is not a product but combines two products to offer an investment solution.

How does STP work?

To understand how STP works, let us take an example. Assume that you receive INR 25 lakh as your share from the sale of an ancestral property. The markets are at historical highs and it may not be the right time to invest in equity funds.

An STP is similar to a systematic investment plan but attractive for investing a lump sum amount. The amount is invested in liquid funds and over a period, a fixed amount is systematically transferred to equity mutual funds.

Importance of liquid funds

Often, you may let your money sit idle in your savings account when you are not sure if the time is right to invest in equity funds. Most banks offer between 4% and 6% interest on savings accounts. In comparison, liquid funds offer higher returns, which can beat savings bank account interest rate by 2% to 5%.

Human nature is uncertain and it is possible that you may spend the funds for other purposes. This erodes the investible surplus and negatively impacts the long-term wealth creation. Parking the funds in liquid schemes ensures the amount is not spent while earning some returns.

Another advantage of parking your funds is rupee cost averaging (RCA). The total amount is periodically transferred from the liquid funds into equity funds, which reduces the average cost. The systematic withdrawal over a period ensures short-term market volatility does not impact your investments and potential returns.